Red Flags of LinkedIn's IPO

Philip Cortes

Philip Cortes

LinkedIn’s shares rose to $100 /share, up from their IPO price of $45 in less than 24 hours. My having a startup in this space has led many people to ask me what I think of LinkedIn – so I dug a little deeper to see what the excitement was all about. What I found was that there were a multitude of red flags, buried deep in the data they presented, and within the market place as a whole.

LinkedIn’s stock value is based on its discounted future cash flows, ergo; your guess is as good as anyone else’s. The two main assumptions driving the DCF model are (users) and (revenues/user), or simply stated:

(Users ) * (Revenue / User)

Based on this formula, LinkedIn’s investors believe growth projections will fall into one of three categories: massive user growth, massive revenue/user growth, or both.

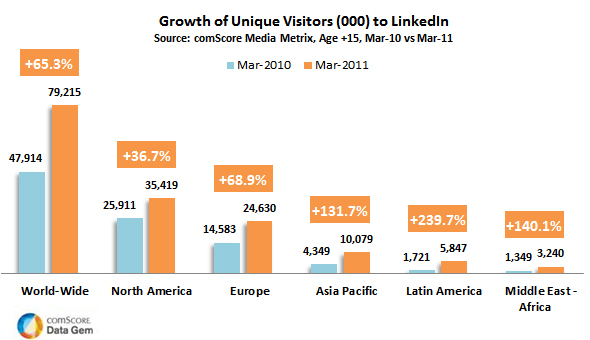

I. User Growth Red Flags:

a) Young people aren’t joining LinkedIn…

LinkedIn seems to have the user acquisition side of the equation pretty well covered. (As we can see here) That having been said, I see a few things that concern me. The first issue is one of demographics. It is not clear that individuals in the 18-25 demographic are joining LinkedIn at the same rate that people in the 27-60 demographic did. Only 20.9% of LinkedIn’s users are 24 and under. (Source) I would argue that a lot of LinkedIn’s growth has stemmed from being an alternative to Facebook for the 27-60 age group. For example, my former boss at Bloomberg is on LinkedIn, but would never even consider joining Facebook.

b) Social and Professional Use Cases are Being Blurred Across Social Networks:

Facebook is no longer about simply “poking” that cutie you just met. The use cases for Facebook are evolving. Whereas Facebook was built as an inherently social tool, the lines of use are starting to become blurred. Recent studies have shown that 1 in 4 Facebook users, and 1 in 3 LinkedIn users use the platforms for “both personal and professional purposes.” I believe the number of people using social networking websites for both personal and professional purpose will only continue to grow, thus allowing Facebook to expand its former niche position among a wide swath of both the younger and older demographic. (Source)

II. Revenue/User Red Flags:

1) Did you know that the majority of LinkedIn users don’t use the site?

Advertising revenue online is based on how often the ads are seen, or clicked on. As per LinkedIn’s own admission in its S-1 filing: “the number of our registered members is higher than the number of actual members, and a substantial majority of our page views are generated by a minority of our members”. This hints at the fact that most people use LinkedIn as a public repository for their online resumes. Unless LinkedIn is able to build a stronger more relevant feature set for the majority of their users, the revenue they make per user on advertising may decrease as users aren’t coming back to the site.

2) 32% of LinkedIn’s revenue is ad driven – this is likely to collapse as they dilute the “quality” of their users for quantity.

|

Hiring |

Marketing |

Premium |

|

|

Percent Of Revenues |

30% |

32% |

38% |

|

Millions |

$16.47 |

$17.568 |

$20.862 |

|

Per User |

$ 0.23 |

$ 0.24 |

$ 0.29 |

|

Per User/Month |

$ 0.08 |

$ 0.08 |

$ 0.10 |

Source: LinkedIn S-1 Filing

Also, I believe that the amount they can capture per user is likely to diminish over time, as their user base won’t be as influential or affluent. Currently, their advertising spin relies on a Nielsen study that found that “U.S. visitors to our website represent more decision makers, have higher average household incomes and are comprised of more college or post graduates than U.S. visitors of many leading business websites. “ Once they begin to capture a greater user base both in the US and abroad, I believe it will also likely result in them having to compress the amount of revenue they can capture for each user.

III. Things to Watch Out For:

1) User Growth:

a. How fast are they acquiring new users, and where is this growth coming from? It’s important to see that LinkedIn is able to displace local competitors, as Facebook was able to do a few years ago. The key markets to watch include Germany (Xing) and France (Viadeo).

Of LinkedIn’s 100m users today, 44 million are in the United States, and 56 million are abroad. They’re seeing massive growth rates from Brazil (428% YOY growth), Mexico (178%), India (76%) and France (72%). As we can see in the infographic below, it seems that they have hit “escape velocity” with their user acquisition in key markets abroad, but itll be important that they maintain that in the near future.

b. How often are these users returning to the site? Keeping a close eye on monthly unique visitors and page views will be a good indicator of how often their new users are coming back to the site, and how much churn there is in old users. This will be a leading indicator of whether they could eventually make more ad dollars per user since they’d be getting more page views and repeat usage, and thus compensating for the dilution in the quality of the user.

2) Feature Set:

What features are they rolling out, and how are they impacting both the virality of the application, and the use cases for their users. It’s clear that the current feature set is powerful for people in Human Resources, and Sales. Outside of those two demographics, it’s not clear that LinkedIn is doing a good job of converting their users to paid services. Adding features could help them create a 4th, 5th or even 6th revenue stream that stabilizes their business and makes their service more defensible.

Acquisitions. There is a flurry of startups trying to tackle different branches of LinkedIn’s revenue, and it’s important for LinkedIn to either move early to acquire those startups with traction, or build a competing feature set.

Connections / User. In our own study at my startup we have found LinkedIn’s social graph to be approximately ½ to 1/3 as broad as that of Facebook’s.

3) Facebook, Facebook, Facebook.

In this case, Facebook isn’t just the 600lb gorilla, it’s the entire jungle. When Facebook launched, it had the option to select “networking” as one of the three things a user is “looking for” on the service. They’ve clearly moved away from professional networking, but it wouldn’t be difficult for them to add LinkedIn’s search feature set, on top of a much more powerful social graph. As noted earlier, the lines between professional and personal use cases on social networks are being blurred, and it’s important to see if Facebook makes any moves into the space.